How Does Settling With an Activist Impact Shareholder Returns?

An examination of post-settlement stock price and M&A outcomes, as well as other implications

Agreeing to a settlement ranks among one of the most consequential decisions a board can face. Settlements typically involve the addition of activist-supported directors, who often bring their own priorities into the boardroom. Increasingly, settlement agreements also call for the creation of special board committees with specific mandates, for example, to oversee a strategic review.

Despite the high stakes, settlements between activist investors and the companies they target appear to be occurring at an ever faster pace. This reflects several factors, including an eagerness on the part of boards and management teams to avoid a distracting and costly public fight. The implementation of the Universal Proxy Card, which many perceive as increasing reputational risk for individual directors facing contested votes, may also be a contributing factor. Activists are similarly motivated to reach quick settlements to minimize costs and the risk of alienating shareholders. Importantly, a settlement often allows activists to move from the negotiation table to the decision table (i.e., the boardroom) and exert influence from the inside.

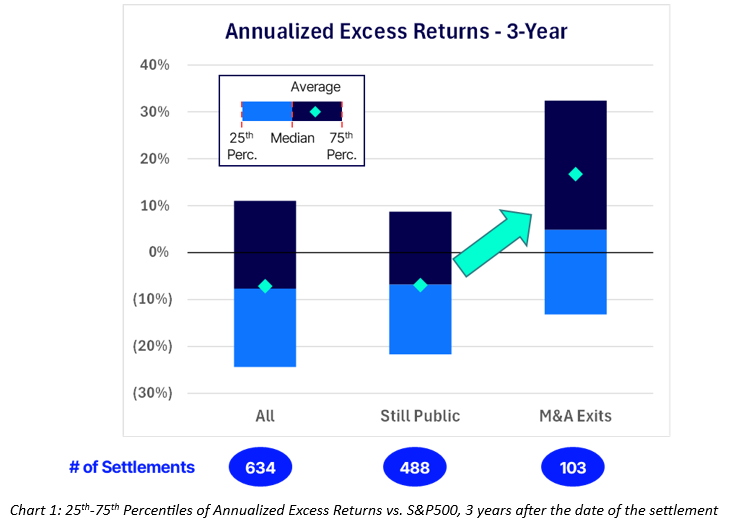

A fundamental question for directors considering a settlement is how the proposed agreement is likely to impact shareholder value. To answer this question, we analyzed 634 settlements entered between U.S.-listed companies and activists from 2010 through the end of 2024. Specifically, we examined stock price performance during the three-year period following the settlement, also taking into consideration whether the company was eventually acquired or remained public.

The results of this analysis offer valuable quantitative insights to help boards more effectively evaluate the potential outcomes of entering into a settlement agreement with an activist.

What happens to a company’s stock price post-settlement?

What happens to a company’s stock price post-settlement?

To measure stock price performance post-settlement, we examined the annualized total shareholder returns for the company in excess of the S&P 500 over a three-year period following the agreement date. We used three years as a reasonable timeframe to measure the potential impact an activist may have on a company’s valuation following a settlement agreement. We also identified instances where the company was sold or went bankrupt during the three-year window.

Our analysis showed that ~60% of companies underperformed the market post-settlement, with the average company underperforming the market by nearly 10%. There are a few potential explanations for this underperformance. Companies targeted by activists may have fundamental issues that drew the activist in the first place and remain post-settlement. Another explanation is that settling with an activist and prioritizing their agenda in the boardroom is inherently disruptive, ultimately weighing down the company’s performance.

The findings of this analysis suggest that settlements do not generate benefits for investors with long-term investment horizons. The exception occurs when looking at companies that were sold within the same three-year period. On average, these companies outperformed the market by more than 15%. This represents a substantial spread to the average of the companies that were still public at the three-year mark, proving that not all companies underperform the market post-settlement.

Although it is not always possible to directly link the sale of a company to the activist’s involvement or settlement, this analysis demonstrates that M&A outcomes offer a far more favorable and reliable path to delivering superior returns.

It’s no surprise that urging a sale process is one of the most frequent demands made by activists. Indeed, the sale of a poorly managed company is generally in the best interest of shareholders. However, directors facing activist demands for a sale process should remember that more often than not, these strategic reviews do not end in a transaction. In fact, two-thirds of companies announcing a public strategic review receive no offers within 12 months, causing double-digit share price declines on average [1] alongside other negative consequences.

How common is a sale of the company after a settlement, and how quickly does it happen?

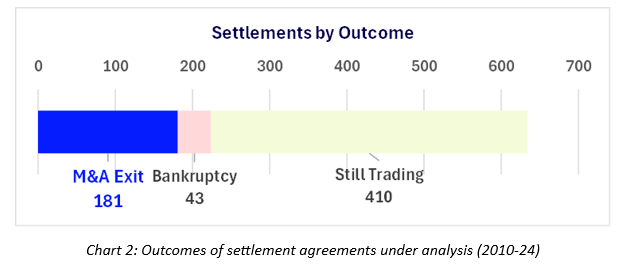

Of the 634 settlements examined, approximately 30% were followed by the company being sold or taken private. Additionally, roughly 7% of companies ultimately filed for bankruptcy or were liquidated.

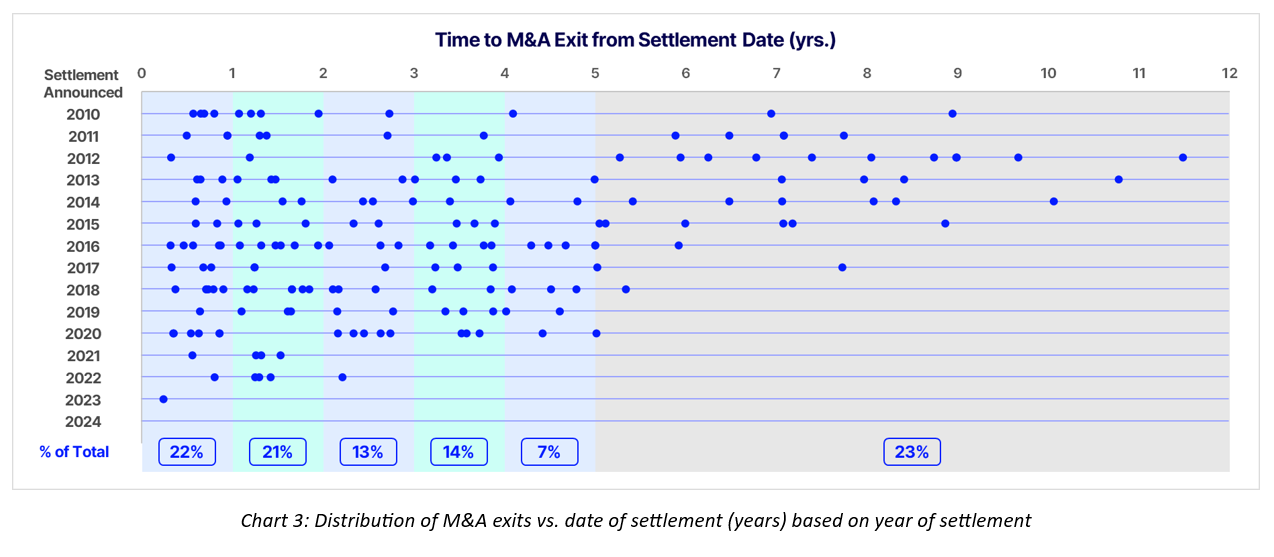

M&A outcomes can materialize quickly after a settlement. In the data we analyzed, a majority of transactions, approximately 55%, occurred within three years of the settlement, 22% within one year, with a few happening in as little as three months. Approximately 23% of transactions occur five or more years after the settlement. In these cases, it’s difficult to argue that the activist involvement or the settlement was the catalyst for the sale.

What else should directors know when considering a potential settlement?

Settling with an activist can carry other consequences potentially detrimental to the company and its shareholders, particularly when a principal from the activist fund joins the board as part of the agreement.

These consequences include:

- A greater likelihood of CEO turnover. Over the past two years, 20% of companies targeted by activists saw their CEO depart within a year of the campaign’s launch, significantly higher than the average annual CEO turnover in the S&P 500 of 12%. [2] In many of these situations, activist nominees on the board helped facilitate CEO departures, even when the fund did not explicitly target the CEO during its campaign.

- Potential disruption to boardroom dynamics. At times, dissident nominees can strengthen oversight and accountability or bring valuable expertise that was previously lacking. In other cases, they can disrupt boardroom dynamics by pushing the agenda of the activist fund, which may not align with the interests of all shareholders.

- An increase in material non-public information leaks. In a study [3] on the effects of settlements where an activist-nominated director joins the board, Former SEC Commissioner Robert Jackson and Columbia Law’s John Coffee found that these appointments increase NMPI leaks by 25% to 27% versus a control group. The research, which evaluated over 600,000 Form 8-K’s filed by nearly 8,000 publicly traded companies, showed that the company’s stock price begins to reflect future still undisclosed business or board updates soon after the activist’s appointee enters the boardroom, particularly if that individual is an employee at the activist fund. The authors conclude the “most plausible explanation” for this pattern is informed trading.

Importantly, directors should understand that a settlement may not deliver lasting peace. As settlement agreements often contain standstills that expire prior to the next year’s director nomination deadline, many activists have waged proxy fights at the same company over two consecutive years, even after securing board representation in the initial settlement.

Even more concerning, activists may not wait until the following proxy season to agitate publicly. In numerous instances, activists under standstills or their advisors have spoken to financial reporters “on background,” i.e., not for attribution, resulting in news articles outlining criticisms of management and members of the board. This can occur when the activist feels the company is disregarding their suggestions or is moving too slowly to implement them. These leaks create the very distraction the board aimed to prevent by reaching the settlement in the first place.

Making an informed decision

Directors and companies face a critical decision when considering a settlement with a shareholder activist. In making this decision, they must balance the practical goal of minimizing distractions and cost with a clearer perspective on long-term outcomes.

This analysis reveals that settling often doesn’t yield positive results. On the whole, post-settlement companies tend to underperform the market, unless they are sold. While this insight may complicate boards’ decision-making, it ultimately provides them with a clearer understanding of how to choose the best path to maximize shareholder value.

Sources: FactSet, 13D Monitor, press reports and publicly available data and sources.

1 Giedt, J. Z. (2023). Economic consequences of announcing strategic alternatives: A voluntary disclosure’s benefits and costs. https://doi.org/10.1111/1911-3846.12880 (go back)

2 Barclays. 2024 Review of Shareholder Activism (go back)

3 Coffee, J., Jackson, R., Mitts, J. and Bishop, R. Activist Directors and Agency Costs: What Happens When an Activist Director Goes on the Board (2019), Cornell Law Review (104)2. (go back)

Methodology:

- Excess returns are calculated as the difference between the annualized 3-year TSR of the affected company and the corresponding performance of the S&P500. Dividends are considered as reinvested.

- For companies that experienced an M&A exit within the 3-year time frame, we assumed that the stock price on the last trading day is a proxy for the sale price paid by the acquiror for the company.

- Companies with an M&A exit beyond their 3-year anniversary were included as part of the pool of still-public companies through the 3-year timeframe; ~45% of post-settlement transactions (~80 settlements) fell under this category

Distribution channels: Education

Legal Disclaimer:

EIN Presswire provides this news content "as is" without warranty of any kind. We do not accept any responsibility or liability for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this article. If you have any complaints or copyright issues related to this article, kindly contact the author above.

Submit your press release